It’s a loan given by a bank or other financial institution for the purchase of a residence or home. In a home loan, the owner of the property (the borrower) transfers the title to the lender (Bank or Financial Institution) on the condition that the title will be transferred back to the owner once the payment has been made and other terms of the mortgage have been met. Home loans consist of a fixed or Floating interest rate and payment terms. that give you the answer to your question which that “What do you need to buy House?

1) Eligibility Criteria:

Housing loan eligibility is the simple way in which banks and financial institutions evaluate your potential to repay the housing loan in due time. There are numerous factors which affect the home loan eligibility for salaried professionals, however, the below-mentioned factors are given high importance. Salaried persons aiming to purchase their dream homes through housing loans must evaluate the same, to ensure they have access to the vital finance for their dream home.

* Age and Income

* Co- applicants income

* Credit Score

* Occupation

* Reputation of Bank or Financial Institution

* Relationship with Bank or Financial Institution.

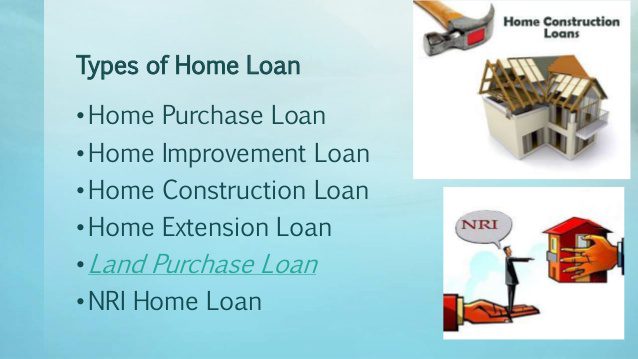

2) Type of Home Loan:

Several Lenders offer home loans, not only for buying a house but also for a variety of other purposes. Some of the popular types of home loans available in the financial market are described below.

* Purchase of Land

* The Home Purchase

* A Construction of House

* Home Improvement

* Balance Transfer of Home Loans.

3) The rate of Interest:

In-Home Loan there are two types of home loans based on the fixed and floating (or variable) rate of interest.

As the name suggests that a fixed rate of interest loan is where the interest rate doesn’t change with market fluctuations.

On the other hand, the Floating rate of interest changes according to the market conditions or fluctuations. For Home loan borrowers it’s better to choose shorter tenure of loan because longer tenure loan causes a high amount of repayment.

4) Saving, Income, and Expenditure:

The applicant of Home loan borrower makes ensure about all their saving, income and expenditure for the purpose of deciding how many loans EMI (Equated Monthly Installment) they can repay. It should be saving and income more than expenditure than the only loan needed loan amount can repay on time.

5) Negotiate the Rate of Interest:

Whichever option you choose, do not forget that you can negotiate on the interest rate. Though the bank would always have an upper-hand, especially if you are an existing customer with a long relationship with the bank. If you have a clean record in your credit history for payments made on time. Use it to negotiate a loan amount and the rate. Every bank wants good business and a high credit score gives you bargaining power. that helps you to buy a house.

6) Credit History:

It contains information regarding whether the customer has any bankruptcies, liens, judgments or collections. This information is all contained on a customer is a credit report. More there credit score means there is no problem for the availing loan facility. which help you to buy a house.

7) Tenure of Loan:

The maximum home loan tenure offered by all major Banks and Financial Institution. The longer the tenure, the lower is the EMI, which makes it very tempting to go for a 25-30 year loan. However, it is best to take a loan for the shortest tenure you can afford. In a long-term loan, the interest outgo is too high. The longer the tenure, the higher is the compound interest that the bank earns.

8) Documentation and Charges:

When you take a home loan, you need not to pay the EMI on the loan. there are as many as different charges, though not all of them apply to every case. Before applying loan get all the fees structure and list of documents should be provided. The major fees are Processing Fee, Technical, Legal Fees, prepayment charges, application fee, administration fee, Technical evaluation fee, Documentation fee, and many others.that helps you to buy a house.

9) Tax Benefits:

Tax benefits are available Under Section 80C of the Income Tax Act, one can avail tax benefits on a principal amount of the home loan. Maximum tax deduction allowed is Rs.1,50,000. The tax deduction is on the payment basis irrespective of the year for which the payment has been made. Here you can read 15 best tax saving methods for 2019.

10) The ability of Repayment:

It pays to be disciplined, especially when it comes to repayment of dues. Whether it is a short term debt or a long-term loan like your house loan. Don’t miss the payment. Missing an EMI or delaying a payment are among the key factors that can impact your credit profile and difficult chances of taking a loan for other needs later in life.one of the best work doing while buy house.

Conclusion: Everyone has dreamed of House. Nowadays house loan is a major financial asset for the bank and financial institutions. The applicant ( Borrower ) of loan should get all information about house loan before applying for the loan and utilize the loan amount for a specific purpose.